Special Report - Look Back on Winter Storm Fern

JANUARY 28, 2026

NATURAL GAS

Pricing

Year to date NYMEX natural gas had been range bound between $3.09 and $3.62/MMBtu. Once Winter Storm Fern started developing and forecasts became more accurate natural gas rallied, eventually peaking at $7.35/MMBtu on Monday, 1/26 when Fern’s impact was felt across most of the country. Meanwhile, Henry Hub hit an all-time daily high of $53.75 and finished the day settling at $30.57.

Basis pricing was highly elevated in regions more severely impacted and those facing congestion issues. For instance, on 1/26, Chicago Citygate settled at $40.67, Algonquin Citygate, servicing MA, CT, RI, NY and NJ settled at $65.48. Transco Zone 5 South serving GA, SC, NC, and VA settled at an impressive $80.51/MMBtu. Rate payers that do not have a hedge or fixed price in place can expect hefty natural gas bills.

Looking Forward

Natural gas has retreated from the highs of January 26, but has support at $6.00 (February contract). The continued elevated pricing is mostly due to a developing storm, and an anticipated historical natural gas inventory draw.

The approaching storm that will impact southern Virginia, the Carolinas, and parts of W. Virginia, Kentucky, and Tennessee starting Friday night where heavy snowfall and high winds are expected. The system will spread further north and east over the weekend, bringing light to moderate snow to eastern New England.

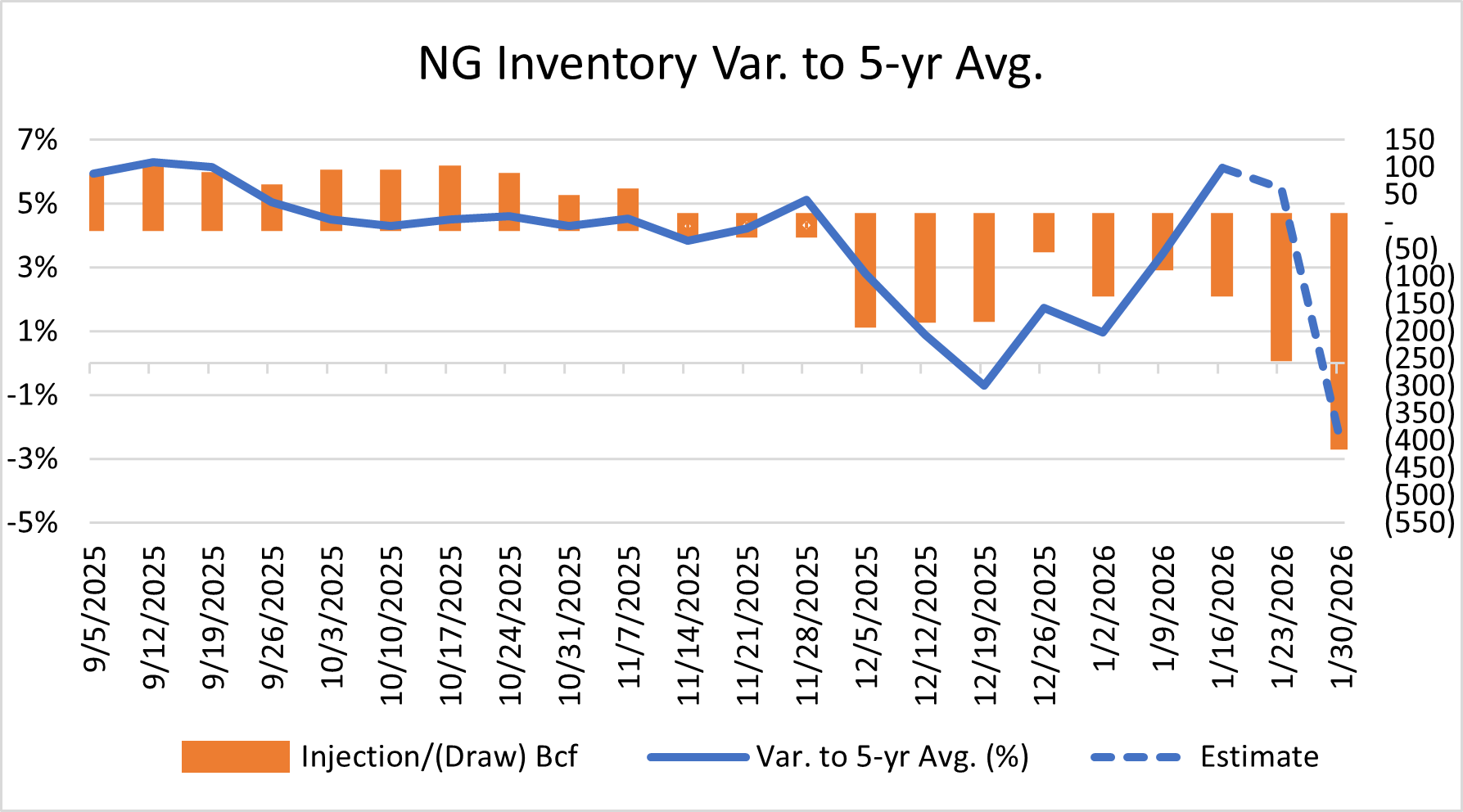

January 29th’s EIA Natural Gas Inventory Report will cover week ending January 23. This report will not cover the full impact of the winter storm. The following week, the February 5 Inventory Report will cover the entirety of Winter Storm Fern. The 1/23 draw is expected to be around 250 Bcf. The 1/30 draw is expected to be around 400 Bcf. This could be a record setting late-January draw. Inventories currently sit comfortably 5% above the 5-yr average and 6% above the year-ago mark. We expect these surpluses to erode to a deficit to the 5-yr average.

January 25 freeze-offs peaked at an estimated 17 Bcf/day. Total impact to production is expected to be ~86 Bcf for the duration of the storm.

As expected, demand was highly elevated. Early estimates are showing 156 Bcf/day at the storm’s peak, whereas the historical average demand in January is about 137 Bcf/day. For context, domestic natural gas production currently sits at about 109 Bcf/day.

The only downward pressure on natural gas would be the considerable drop in LNG feedgas during the storm. The decrease is estimated at 30%, dropping from 17.5 Bcf/day to 12.25 Bcf/day. Feedgas was throttled as natural gas was redirected for domestic use during the storm, where it was sold at a considerably premium.

PJM

January 25 the US Department of Energy issued an emergency order for both ERCOT and PJM. The emergency order allowed generators to temporarily exceed permitted air quality and other environmental limitations. An emergency order allows coal, natural gas, and oil-fired units to run at higher output for longer without violating their permitted allowance or facing penalties.

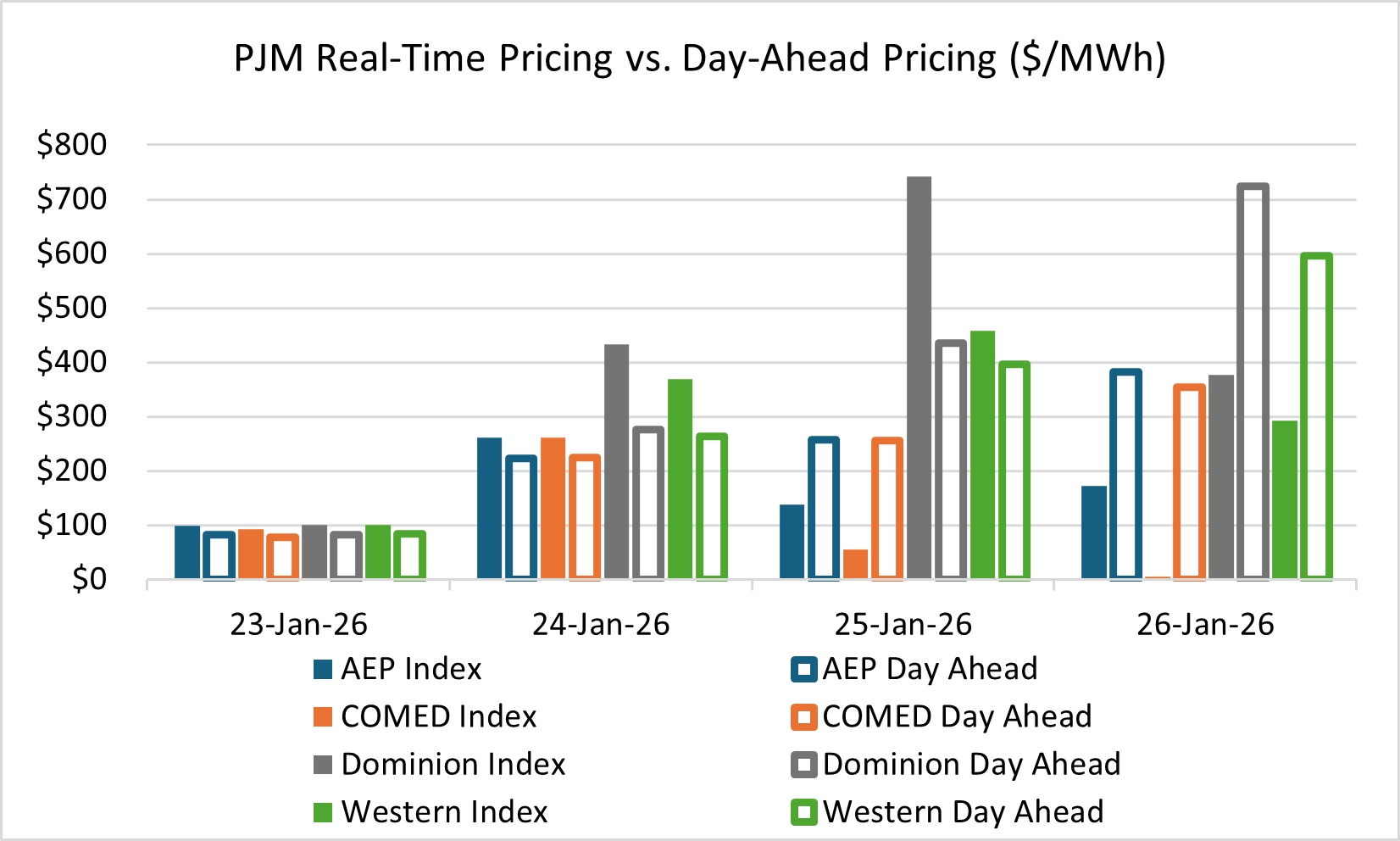

PJM, the US’s largest regional transmission organization, did considerably well during the extreme cold. PJM avoided widespread rotating blackouts or major load shedding, maintaining reliability under extreme condition. However, the event exposed vulnerabilities: scarce supply margins, gas supply issues, and reduced flexibility from retirements in conjunction with demand surges. Localized outages occurred from ice on lines, contributing to >1 million total U.S. power outages during the storm, but PJM's system held without the failures seen in past events like Uri (2021) or Elliott (2022). Wholesale prices surged dramatically (e.g., $400–700/MWh in PJM and nearby regions), reflecting tightness. PJM had an estimated >100,000 customers lose service during the storm. PJM generation outages peaked January 26 with about 22GW of total outages, 19.71GW being unplanned.

Dominion saw particularly elevated real-time pricing/index pricing. Dominion services Northern Virginia (aka “Data Center Alley”) where there has been tremendous growth in recent years. Dominion faced generation and transmission challenges with the unseasonably cold weather. Natural gas-fired plants were the main culprit of lost generation with frozen equipment, pipeline delivery issues, and fuel supply restrictions.

ERCOT

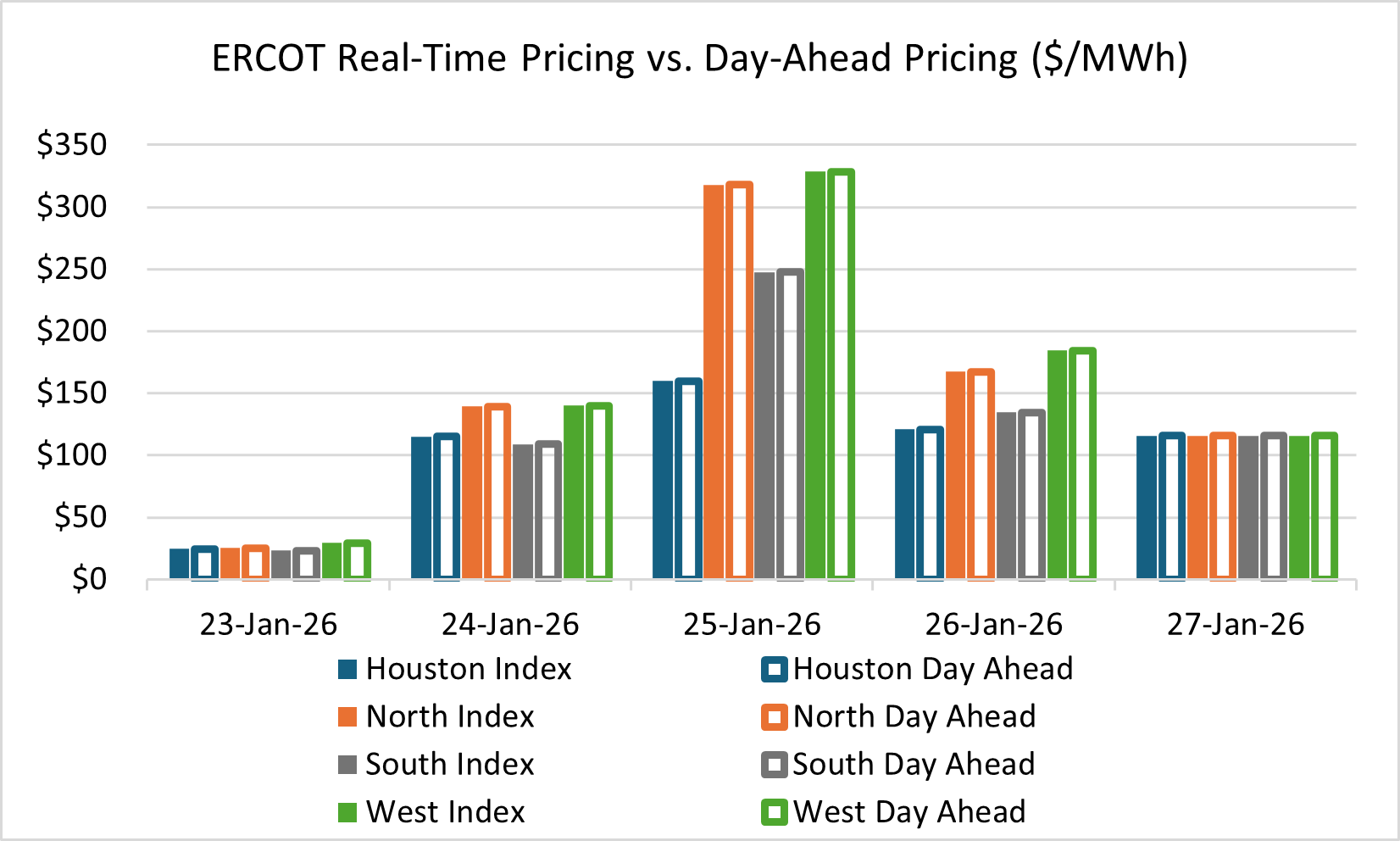

ERCOT performed well during Winter Storm Fern. Real-time pricing was not as volatile as other parts of the country. Interestingly, when compared to PJM, we can see pricing in the day-ahead market was far tighter bound to real-time pricing. This is indicative of better load forecasting, less unplanned outages, and favorable actual weather vs. forecasts.

ERCOT forecasted a peak demand of 83GW. Initial estimates suggest the peak was about 76GW.

ERCOT faced some natural gas restraints but coal and batteries did well, filling the gaps and minimize pricing volatility. Pricing volatility peaked January 25. The North Zone (DFW) experienced high volatility as this zone was the most impacted region in Texas. Real-time prices peaked at $1,148/MWh the evening of the 25th and finished the day averaging $318/MWh. ERCOT’s peak pricing coincided with peak generation outages, about 11.5GW.

In summary, ERCOT performed robustly during Winter Storm Fern—avoiding disaster through post-2021 improvements, proactive alerts, federal emergency support, and a more resilient generation fleet—while handling elevated demand and cold-weather challenges effectively. It was a positive contrast to Uri, demonstrating progress in grid winter readiness, though ongoing risks from gas dependency and extreme events remain.