Infinity Insights - Volume 16, Volume 4

MONTHLY UPDATE - MAY 2026 EDITION

NATURAL GAS

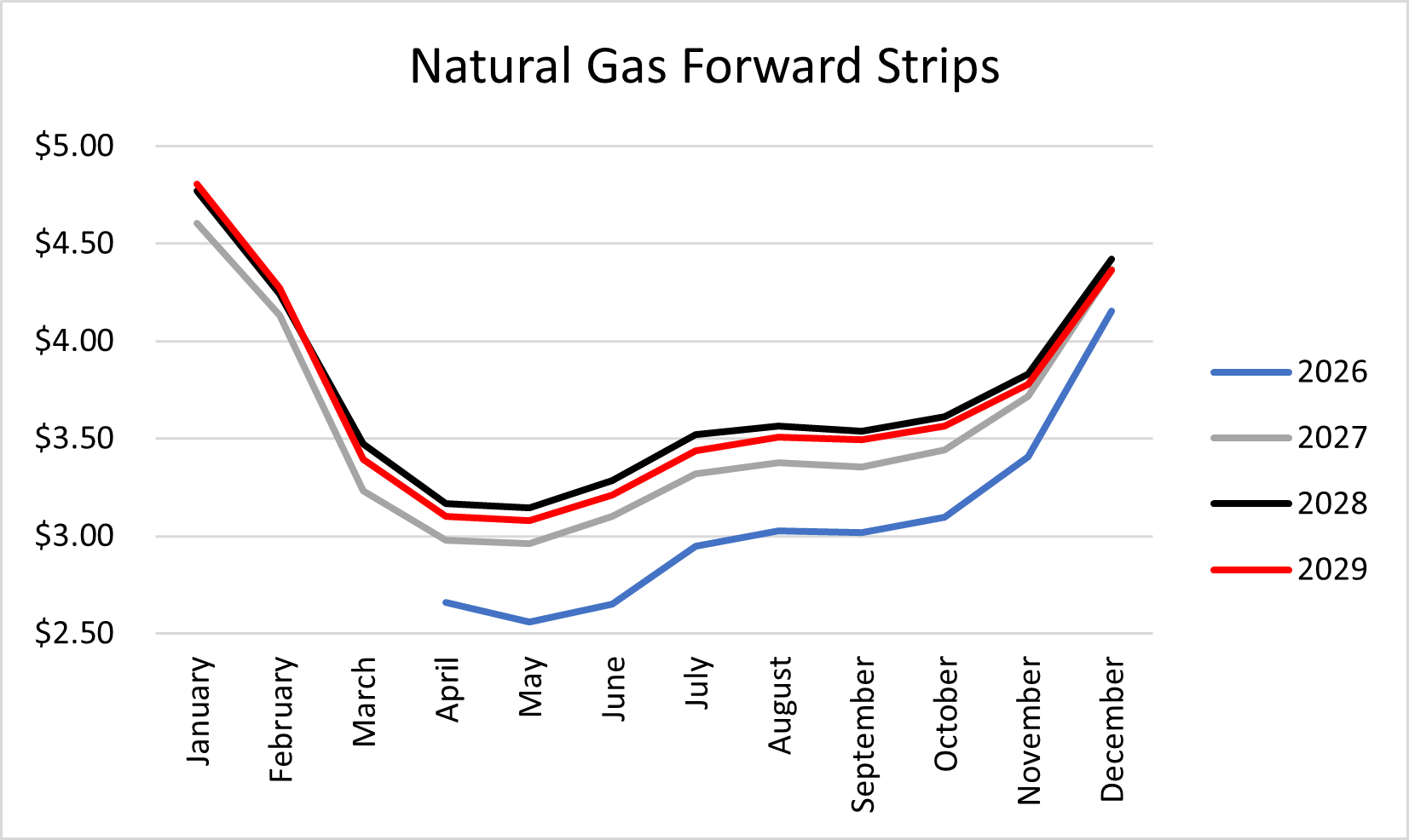

Spot NYMEX Natural Gas hit a 52-week low 4/28, trading around $2.70. Spot has been especially bearish on stout inventories, strong production and mild weather. The discount can be seen impacting the front of both power and natural gas curves. Since our last publication balance year 2026 is trading at an 11% discount, 2027 a 9% discount and 2028 a 4% discount.

Production is at record levels averaging over 108 Bcf/day YTD, a 4% increase YoY. We expect production to continue increasing as LNG liquefaction demand continues to grow. We expect further production if oil prices remain elevated, which will in turn increase oil production and bring more associated gas to market. From April 17th to 24th US rig counts increased from 125 to 129.

Week ending 4/24/26 natural gas inventories increased 79 Bcf, vs. a 5-yr avg. of 63 Bcf for the same week. Inventories currently sit at 6% above the year ago mark and 8% above the 5-yr avg. With an early start to injection season this year due to mild weather, the EIA is forecasting inventories to reach 4,015 Bcf before the start of winter 26/27, 6% greater inventory volumes than the 5-yr average.

Spot natural gas has support at $2.50 with resistance at $3.00.

Balance year 2026 finds support at $2.56 with resistance at $4.16. Calendar year 2027 has support at $2.97 with resistance at $4.61. Calendar year 2028 has support at $3.14 with resistance at $4.77 – across the board, considerably less than our previous publication.

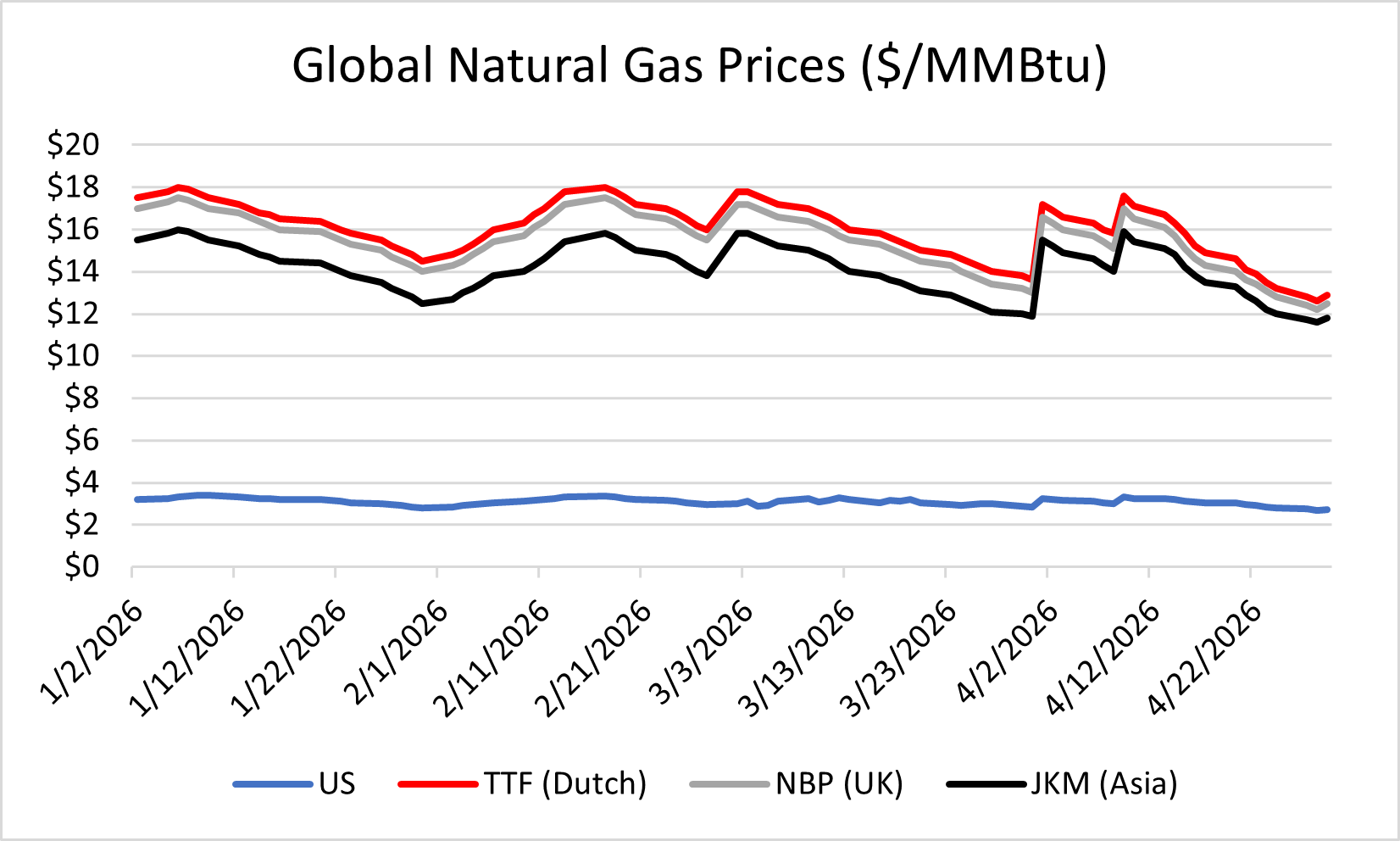

Global natural gas prices ($/MMBtu):

Henry Hub (USA): $2.65↓

NBP (UK): $14.49↓

TTF (Dutch) $13.93↓

JKM (Japan/Korea) $16.48↓

Global natural gas prices have retreated considerably with the announced ceasefire in the Middle East, along with exiting the highly volatile heating season.

Weather

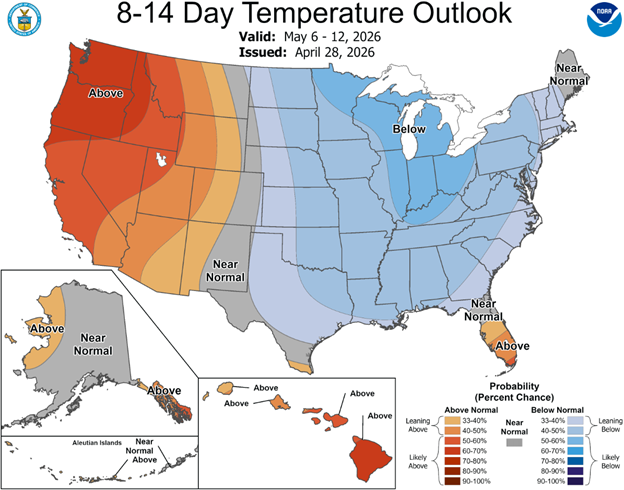

The 6-10 Day and 8-14 Day Temperature Outlooks show below normal temperatures in the east and above normal temperatures in the west, not particularly impactful at this time of year. Current drought conditions are showing exceptionally dry conditions in Colorado, Wyoming, Georgia and Florida. The Precipitation Outlook looks favorable and should provide relief to these areas in the 6-14 Day Outlook.

NOAA’s seasonal outlook for summer 2026 is showing near normal temperatures for the Great Lakes and Midwest regions. The Northwest, Southwest and South are expected to have a warmer than normal summer.

Data Centers Moving Behind the Meter

As data center demand soars and utility interconnection requests swell, companies with the resources are circumventing the interconnection queue by providing their own power generation, a popular concept often referred to as BYOP, bring your own power or behind the meter generation. Behind the meter power generation refers to on-site power generation that supplies a data center without utilizing the traditional utility grid and its metering infrastructure. In the past, behind the meter generation was limited to backup diesel generation. In certain data center hotspots, such as Northern Virginia, interconnection queues have ballooned to 5-7 yrs.

Todays behind the meter data centers’ power sources are diverse, including natural gas, nuclear, and solar power generation, although natural gas has proven to be the dominant power source. This is mainly due to speed to market and current favorable fuel prices.

The obvious and greatest benefit to hyperscalers in the current environment is speed to market. An additional benefits is reliability. Modern hyperscalers are looking for five 9’s reliability, meaning 99.999% of the time their equipment is able to run. Five 9’s works out to about 5 minutes of downtime per calendar year. Another benefit is cost predictability. Hyperscalers know the cost of their generation while eliminating transmission and delivery costs – often a large portion of power costs.

McKinsey is forecasting between 25% and 33% of all new generation for data centers will be behind the meter. Others have speculated by 2030 27-38% of all data centers will rely on some level of on-site primary power generation.

Oracle’s Project Stargate in Abilene, Texas will provide 2.3 GW of behind the meter natural gas generation, expected to be fully operational by mid-2026.

xAI’s Colossus in Memphis, Tennessee originally used mobile natural gas generating units. The EPA later determined the mobile generation units required air permits. Colossus 1 and 2 are already fully functional. Colossus 3 is expected to be complete and operational by the end of 2026. Colossus will have a dedicated 1.2 GW gas power plant and Tesla’s Megapack storage system for battery power.

Switch’s Citadel Campus in Nevada is online with plans to expand to 127 MW of solar and 240 MWh of battery storage. The Citadel Campus is a standout from other hyperscalers with 100% renewable generation.

Hyperscalers’ behind the meter generation is gaining momentum and becoming more widespread. As long as regulation remains a major stumbling block with today’s utilities, we expect to see the trend accelerate. If regulation adapts to this new reality, we could see hyperscalers curtailing and providing power to the grid. Currently, the regulatory environment makes it too cumbersome for hyperscalers to help energize the grid. It would be interesting to see a scenario where hyperscalers could be incentivized through pricing to curtail usage and help support our grid.

Tennessee Embracing Nuclear

Tennessee is making a strategic push to position Oak Ridge at the center of America’s next wave of nuclear energy development. April 2, Governor Bill Lee along with state leaders, outlined a vision to transform the region into a comprehensive hub that supports the entire nuclear lifecycle, from fuel production and advanced reactor design to waste management and recycling.

At the heart of the effort is a proposal to establish a “Nuclear Lifecycle Innovation Campus” in Oak Ridge, leveraging the area’s deep roots in nuclear research and its existing infrastructure. The initiative aims to bring together public and private partners to accelerate the deployment of next-generation technologies, including small modular reactors (SMRs) and other advanced designs.

The Tennessee Valley Authority (TVA) is expected to play a central role, supported by significant federal funding (~$400 million) to help advance new nuclear projects. This aligns with broader national goals to strengthen domestic energy security, reduce reliance on foreign fuel sources, and meet rising electricity demand with low-carbon generation.

State officials emphasize that Oak Ridge is uniquely suited for this role due to its legacy of nuclear innovation, dating back to the Manhattan Project, as well as its concentration of scientific talent and growing interest from private industry. By consolidating research, manufacturing, and deployment capabilities in one location, Tennessee hopes to attract billions in investment and create a new generation of high-skilled jobs.

Ultimately, the initiative is about more than regional economic development—it reflects a broader ambition to reestablish the US as a global leader in nuclear energy, at a time when demand for reliable, carbon-free power is rapidly increasing.

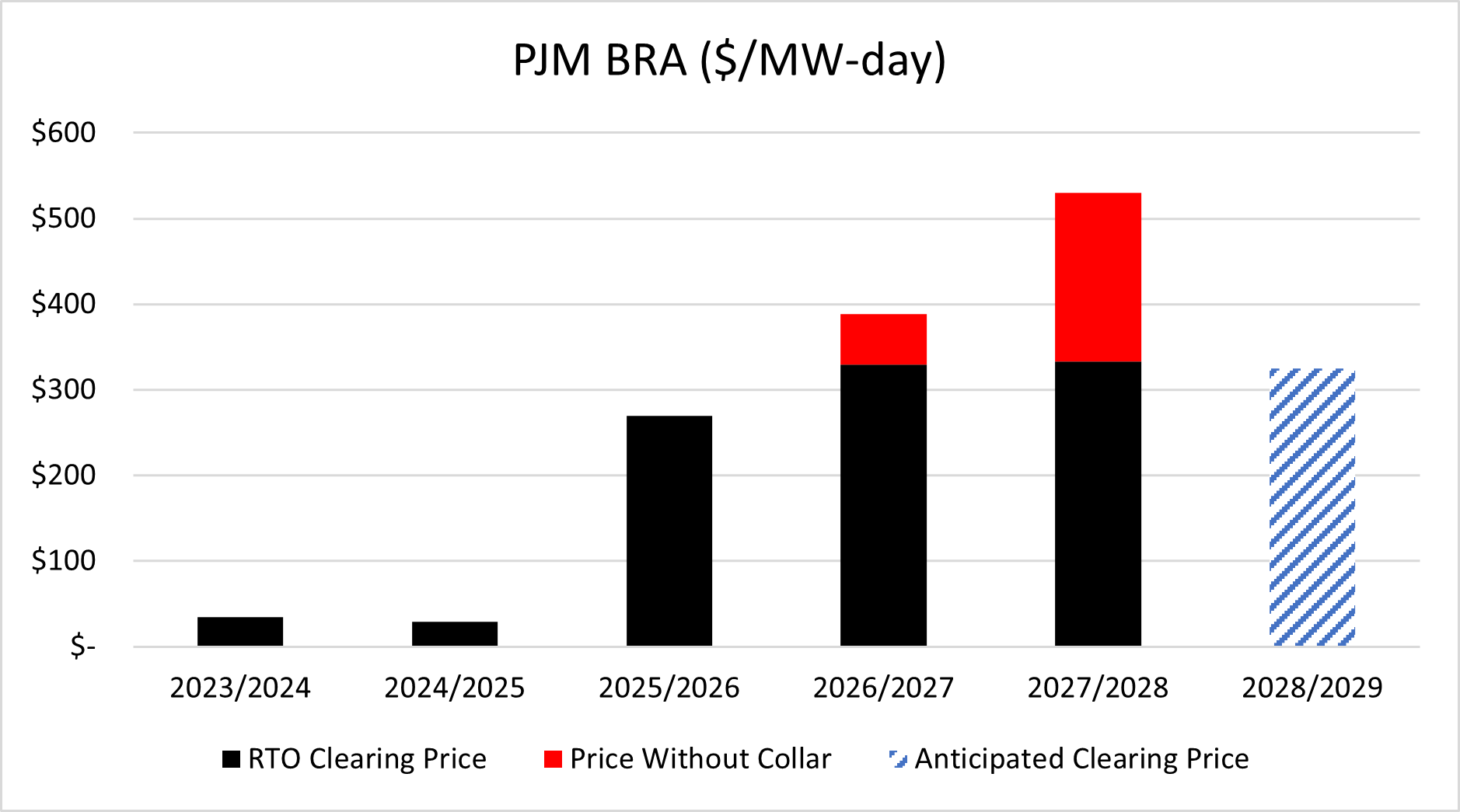

PJM Base Residual Auction

PJM Base Residual Auction (BRA) is scheduled to open June 30, close July 7, and publish results July 14. The BRA sets capacity pricing for all of PJM. Historically, the BRA was an open auction with no limits on pricing. For calendar years 23/24 the BRA cleared at $34.13/MW, calendar year 24/25 the BRA cleared at $28.92, then for 25/26 deliveries the BRA cleared at an astounding $269.92. As a result of the 9X increase in cost pricing collars were introduced for the 26/27 deliveries auction. The auction results were (as expected) at the price cap of $329.17/MW. The same thing happened with 27/28 deliveries, where the price cap was moved slightly higher to $333.44/MW and the auction results were once again at the cap.

The pricing collar or pricing caps have been highly effective in keeping prices in check. 26/27 deliveries which cleared at $329.17 (at the cap) are speculated to have cleared at $388.57, or 18% higher if there had not been a cap in place. 27/28 deliveries cleared at $333.44, once again at the cap, with speculation the auction would have cleared at $529.80, or 59% above the clearing price in absence of the pricing collar.

February 27, PJM proposed an order to extend the pricing collar for the BRA for 28/29 and 29/30 delivery years. April 28 FERC issued an order in Docket ER26-1556 accepting PJM’s proposal to extend the pricing collar. The extension is well received by most PJM states, load interests, and utilities. Some generators have voiced opposition as the collars make the capacity far less lucrative. The price cap is expected to be $325/MW, with most analysts anticipating the auction to settle at or near the cap.

Market News

March CPI ticked up to a seasonally adjusted annual rate of 3.3% vs. 2.4% in February. The increase was driven mainly by the broader energy sector increasing 12.5% and specifically, gasoline prices increasing over 21%. Real GDP grew at 2% annualized, up considerably vs. Q4 2025, but below consensus estimates of 2.2-2.3%. Soft GDP prints put downward pressure on treasury yields since soft GDP results could make a case for future rate cuts. On Wednesday the Federal Reserve left rates unchanged, 3.5% - 3.75%. March unemployment slipped from 4.4% in February to 4.3% in March. Equities are strong, trading around all-time highs.