Infinity Insights - Volume 14, Issue 1

MONTHLY UPDATE - JANUARY 2024 EDITION

NATURAL GAS

NYMEX Natural Gas has settled to the $2.25 range with the most recent EIA Weekly Natural Gas Storage Report showing a net withdrawal of 154 Bcf week over week, whereas consensus estimate was a withdrawal of 164 Bcf. Prices have fallen significantly after much volatility mid-month with the forecast and arrival of Winter Storm Heather.

Note: most recent natural gas inventory report was for the week ending 1/12/2024 and does not capture high usage during the winter storm. Inventory report covering the winter storm period will be available Thursday, January 25.

Spot month natural gas support at $2.35 with resistance at $3.30.

Calendar year 2024 finds support at $2.40 with resistance at $3.60. Calendar year 2025 has support at $3.16 with resistance at $4.23.

EIA provided the following long-term outlook on natural gas. In summary:

2024 expected price to average $2.70/MMBtu, close to current prices

2025 expected price to average $3.00/MMBtu, attributed to LNG export facilities coming online

Natural gas prices remain at historic lows.

WEATHER

After a warmer than normal start to winter US was overwhelmed with the cold brought on by Winter Storm Heather. Looking forward, conditions will return to a mild winter with most of the country expecting warmer than normal conditions. Most recent weather updates have put downward pressure on natural gas prices after climbing before and during Winter Storm Heather.

MARKET NEWS

Special Report: Look Back on Winter Storm Heather

Most of the country was inundated with extremely cold weather the week of January 15. The winter storm was caused by an unstable polar vortex that allowed cold Arctic air to move south, covering most of the US.

Service Interruptions were highly limited. Jackson Prairie Underground Natural Gas Storage Facility serving the Pacific Northwest, south to New Mexico was completely offline Saturday, 1/13 and restored later that evening.

EPCOR reported low or no pressure for customers in Northwest Houston 1/15. The issue was resolved a few hours later.

The Texas grid performed flawlessly. There were localized outages caused by high winds but no grid failures. ERCOT set new records for winter peak demand 1/15 and 1/16 at 76K MW and 78K MW respectively. Above mentioned record winter demand was likely less than the demand during Winter Storm Uri, but due to outages the actual demand could not be measured.

Let’s take a closer look at January 16 when the grid experienced record demand.

ERCOT’s resilience during this event is attributed to:

ERCOT and the PUC’s winterization rules mitigating natural gas service interruptions

Natural gas carried the lion’s share of generation as expected, generating 58% of the grid’s power through the day

Generation Outages remained consistently low

Wind and solar performed

Renewables accounted for 18% of ERCOT’s generation through the day

Solar generation set a new generation record of 14,836 MW

Newly deployed Battery Power Storage performed

Power Storage accounted for .3% of grid generation through the day

More interestingly, battery storage deployment generated 1.8% of the grid’s power at its time of most scarcity

Battery Power Storage is establishing itself as a reliable, easily deployable peak generator

PJM Energy Transition

PJM released a report forecasting thermal generation retirement and anticipated new generation to keep up with growing demand. The report references policy-driven and economic reasons for the anticipated retirements. By 2030 40 GW of thermal retirements are expected. Between 56 – 111 GW of new solar and wind generation are forecasted to come online by 2030. Natural gas generation will be used to fill the gaps between retirements and new generation. PJM’s total forecasted load growth is approximately 1.5% annually. Load growth is attributed to electrification and the growth of data centers.

Click here for the full report.

PJM Winter Preparedness

Winter Storm Elliot, December 21 through 26, 2022, was a catastrophic cyclone that caused blizzard conditions through much of the US as well as Canada. In total, the weather system resulted in approximately 6.3 million customers losing power at some point and approximately 100 deaths.

Subsequently, PJM has released it’s Winter Storm Elliott Event Analysis – click for more information.

In summary, PJM in conjunction with the Federal Energy Regulatory Commission (FERC) has made 30 specific recommendations to enhance generator reliability through seasonal reporting requirements, improved short-term and long-term extreme weather trends, and taking corrective action for generators who were unable to perform during the weather event.

ERCOT Interstate Connection

ERCOT has announced plans to connect the Texas grid with Louisiana and Mississippi through a project called Southern Spirit Transmission. ERCOT currently has the transmission capacity of approximately 1,200 MW through existing interstate connections. Southern Spirit Transmission would increase the transmission capacity by 2,000 MW. To put this into perspective, 2,000 MW is only about 2% of ERCOT’s record peak demand. The project is expected to come online by 2029.

Our take: Although the transmission capacity may seem de minimis, in the event of a catastrophic weather event (Winter Storm Uri), the additional 2,000 MW could power an additional 400,000 homes at any given time. Maybe more importantly, the project indicates a change in ERCOT’s posture away from energy isolationism, which could further stabilize the grid through future interstate projects. Another point worth noting, Southern Spirit Transmission’s plan for lines spanning 320 miles puts ERCOT in a far better position by simply covering more land mass capable of producing and transmitting power and thereby mitigating much risk associated with regional weather systems.

GEOPOLITICS

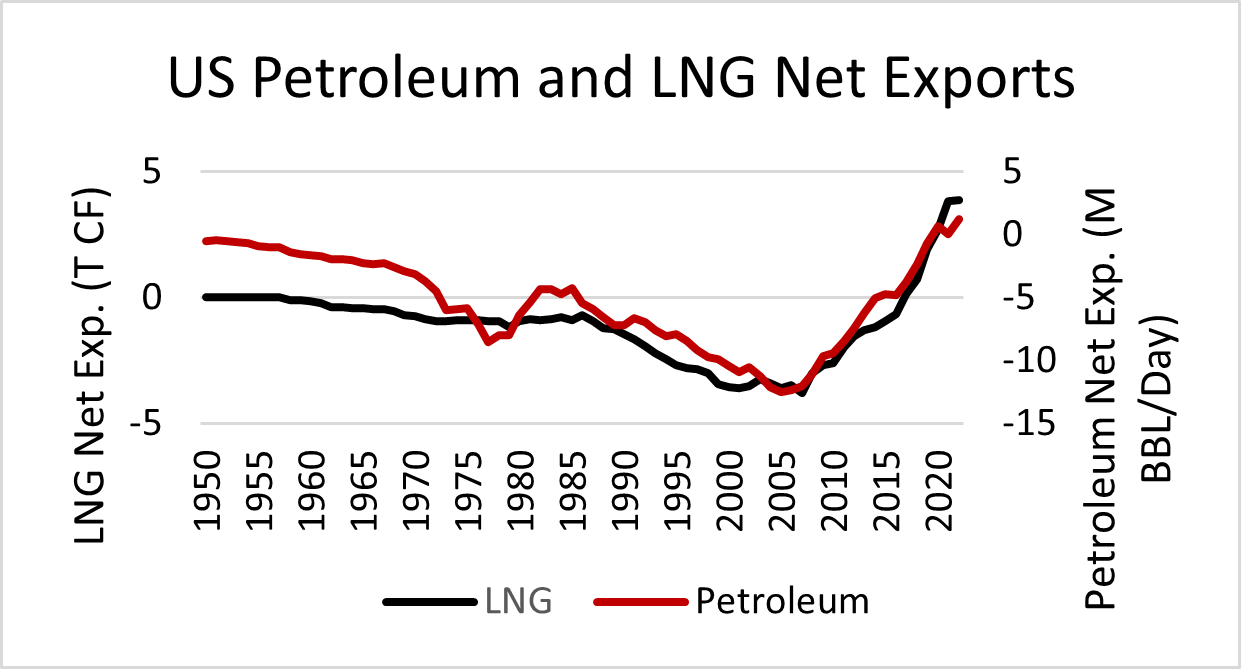

Middle East Tension Impacting Logistics & Energy

As tensions in the Middle East continue to escalate shipping routes are being diverted and could have a material impact on energy markets. According to Lloyd’s, daily Red Sea transits have gone from 386 to 315 daily transits, a 19% reduction. The Suez Canal accounts for 12% and 8% of global crude oil and LNG shipments word-wide respectively. Further disruptions in the region could result in supply issues for much of Europe and Asia. The US finds itself in unique territory as the US is recently a net exporter of both LNG and crude oil. This “energy independence” insulates much of the US from the regional risk. Although, as we saw in early 2022 with the Russia-Ukrainian War, supply in Europe and Asia impact domestic prices as exports become more lucrative. Currently, NYMEX natural gas sits at about $2.40/MMBtu, while Dutch TTF is at $9.08/MMBtu, UK NBP is at $8.86/MMBtu, and Japan/Korea is at $9.59/MMBtu.