Infinity Insights - Volume 15, Issue 19

MONTHLY UPDATE - NOVEMBER 2025 EDITION

NATURAL GAS

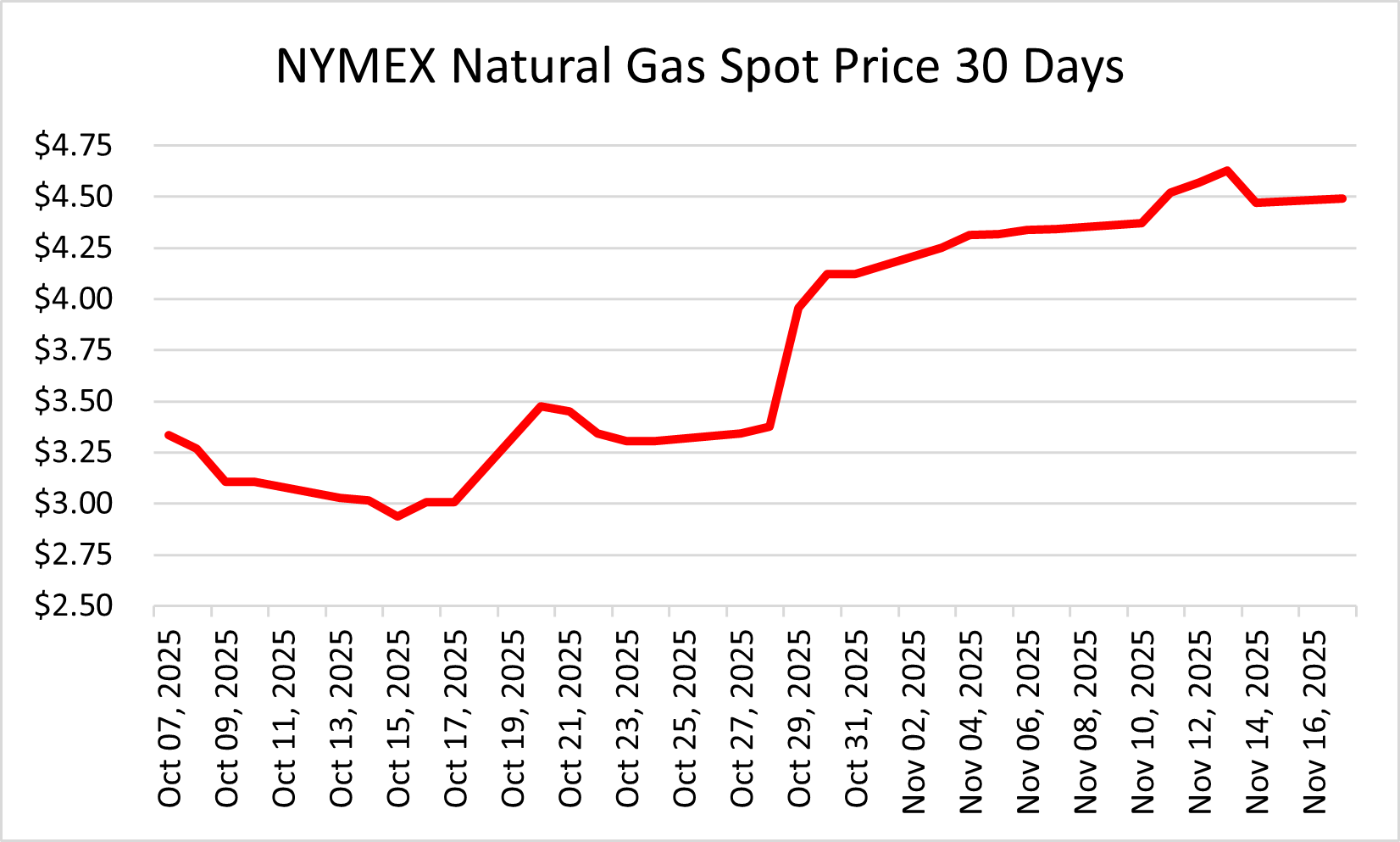

Spot NYMEX Natural Gas is showing support at $4.15 and resistance at $4.70. Spot natural gas gapped up November 24 upon the November 2025 contract expiring. Upon expiration, prompt switched to December 2025, a far more volatile month, which is consistent with historical performance.

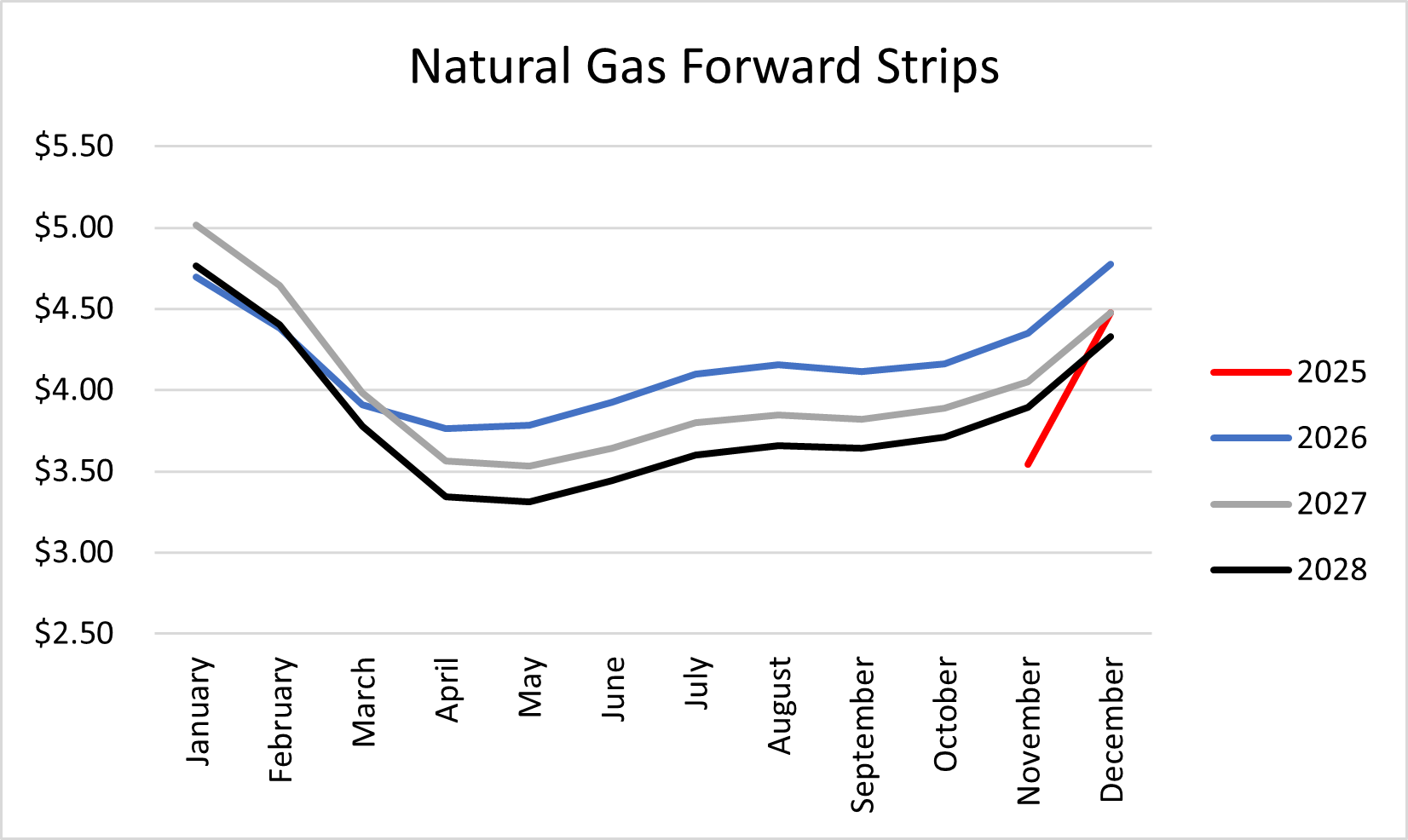

Forward strips balance year 2025 is up 3%, ‘26 up 5%, ‘27 up 3% and ‘28 up 1% versus our prior publication. Forward strips at the front of the curve are up considerably, with calendar year 2026 leading the charge and the outer years far less impacted.

Weekly US natural gas rig count is up 23% year-over-year at 125. Rig count peaked in August 2025 then fell to 117 in September and is seen as plateauing and stabilized at 125. Production has remained strong, around 108.6 Bcf/day. Q4 2025 production is expected to reach 109.2 Bcf/d, ending the year averaging 107.7 Bcf/d, far exceeding the 2024 average of 103.2 Bcf/d.

Current storage inventories sit at .2% below the year-ago mark and 4.5% above the 5-yr average.

EIA’s latest Short-Term Energy Outlook is forecasting natural gas to average $3.90/MMBtu in November through March and $4.00/MMBtu in 2026 – this is a significant reversal from the prior Short-Term Energy Outlook.

Spot month natural gas has support at $4.00 with resistance at $4.75.

Balance year 2025 finds support at $3.50 with resistance at $4.50. Calendar year 2026 has support at $3.76 with resistance at $4.73. Calendar year 2027 has support at $3.53 with resistance at $5.02.

Global natural gas prices ($/MMBtu):

Henry Hub (USA): $4.34↑

NBP (UK): $10.95↑

TTF (Dutch) $10.70↓

JKM (Japan/Korea) $11.00↓

Weather

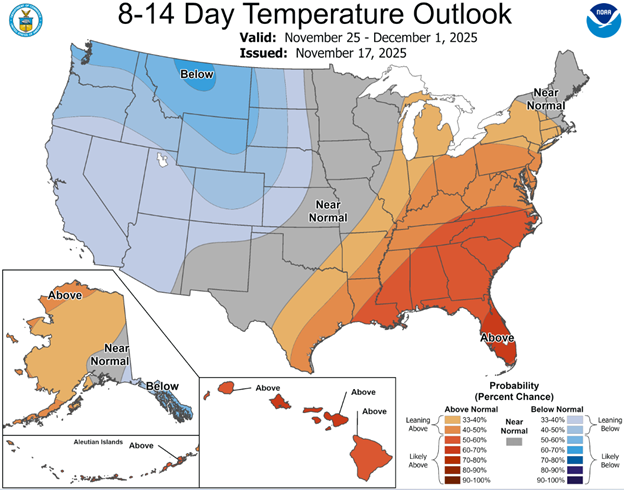

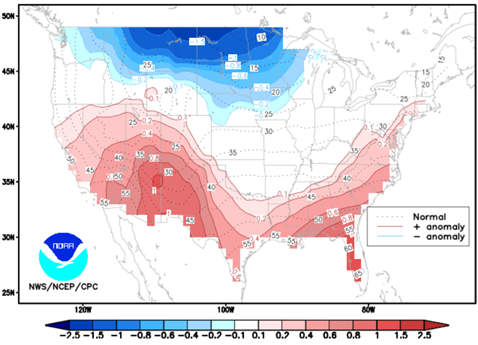

The 8-14 Day Temperature Outlook shows the lower 48 split in half with the west expecting colder than normal temperatures and the east above normal temperatures. The 6-10 Day Temperature Outlook is mostly red across the board. It will be interesting to see if the 8-14 Day Temperature Outlook actually materializes and brings cold weather to the west. The seasonal forecast, which is becoming more precise with growing confidence at this time of the season, is indicating a warmer than normal winter for the southern US and the potential for unseasonably cold weather in the northwest.

Note: on a population weighted basis this points to a mild winter as the heavily populated East and Midwest are expecting above normal temperatures.

Georgia Election – PSC Appointments

On November 4, 2025, in a pivotal off-year special election, Democrats Alicia Johnson and Peter Hubbard secured decisive victories over Republican incumbents Tim Echols and Fitz Johnson, respectively, flipping two seats on Georgia's Public Service Commission (PSC). This marks the first Democratic win for a statewide constitutional office in Georgia since 2006. The PSC, a five-member body, oversees major utilities like Georgia Power, directly influencing residential energy rates, grid reliability, and energy policy. The outgoing Republicans had approved six rate hikes in the past two years, adding roughly $500 annually to the average household bill, fueling voter backlash.

The election signals a potential paradigm shift on the PSC toward prioritizing affordability and renewable energy over unchecked utility expansions. Hubbard, a clean energy advocate, has vowed to "lower utility costs" and "bring more clean, reliable energy resources" to Georgia, potentially accelerating transitions to solar and wind while scrutinizing fossil fuel subsidies. Johnson, emphasizing public interest, aims to refocus the commission on "everyday people, not multi-billion dollar companies," which could lead to stalled or reversed rate increases and greater transparency in utility approvals. Environmental groups like the Sierra Club celebrated this as a "monumental victory for... affordable, clean energy," predicting a "seismic change" in the state's energy landscape that aligns with national trends where 75% of Americans worry about rising bills. However, critics like defeated incumbent Fitz Johnson argue Democratic policies may undermine grid resiliency and business development, potentially sparking legal challenges from utilities. For Georgia's 2.7 million Georgia Power customers, the new commissioners represent a backstop against unchecked rising bills.

At IPP we see this result as a reaction to the disaster that is the expansion of Georgia Power’s Vogtle Electric Generating Plant units 3 and 4. As noted in previous editions, the most recent addition to the US nuclear fleet experienced about 2 years in delays and $16B in cost overruns, a considerable setback for the nuclear industry for the county.

Market News

Unemployment is expected to tick up to 4.4% according to the Chicago Fed. Current official numbers are unavailable as a result of the recent government shutdown. Official unemployment reporting will resume November 20. US 10-yr treasury yield is down to 4.13%, a considerable reduction from mid-January peak of 4.80%. There is a 45% chance of a 25 bps Fed interest rate cut in December and a 54% chance of no change. Equity markets have retreated slightly from late-October highs, down about 3%. Year-to-date equity is up 13%. USD has rebounded from mid-September lows.

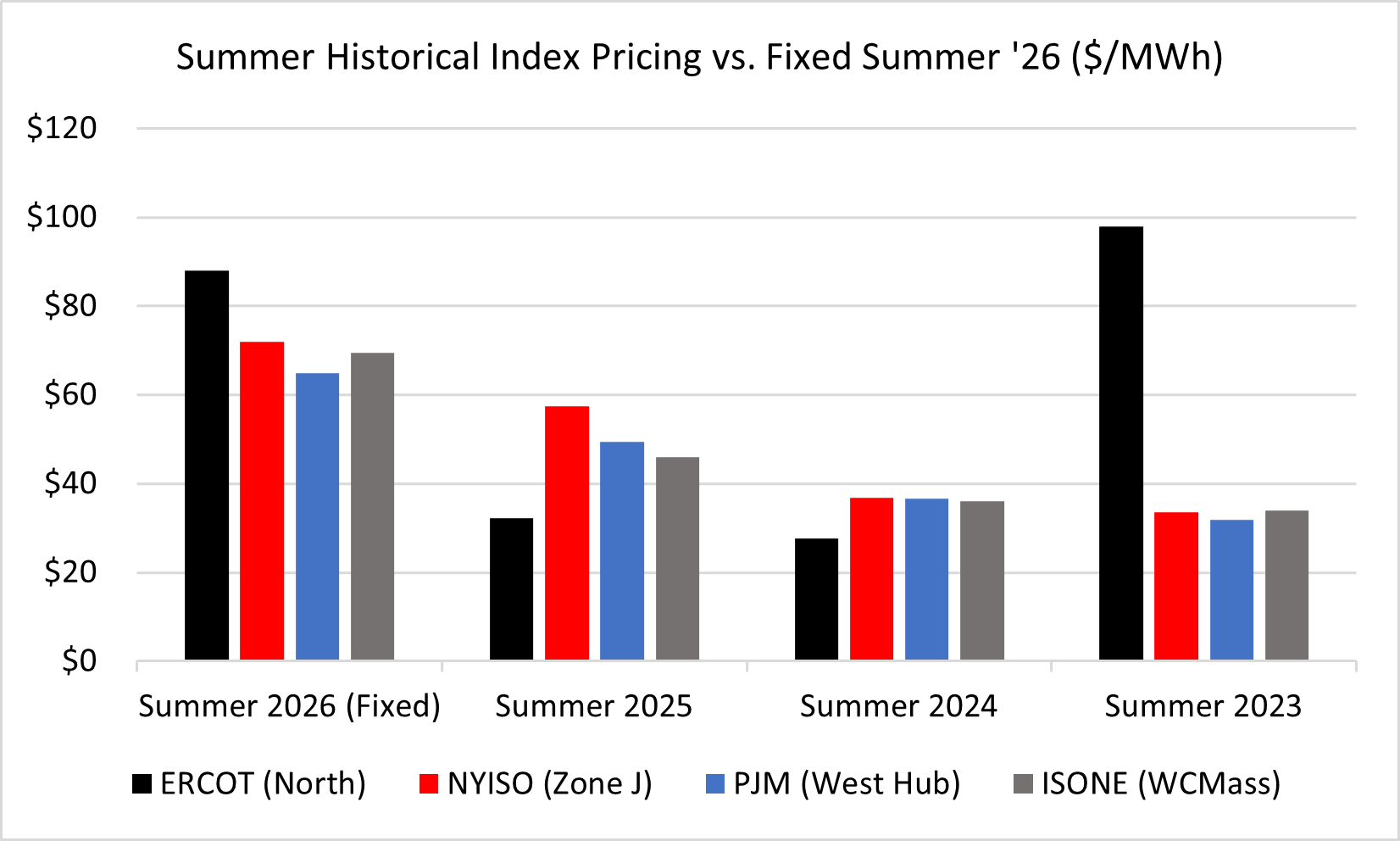

Look Back at Summer 2025

After a considerably volatile summer and muted fall for most of the US, we’ve seen an unexpected, relentless rally in spot natural gas. The recent rally in conjunction with a volatile summer has pushed power pricing higher across future strips.

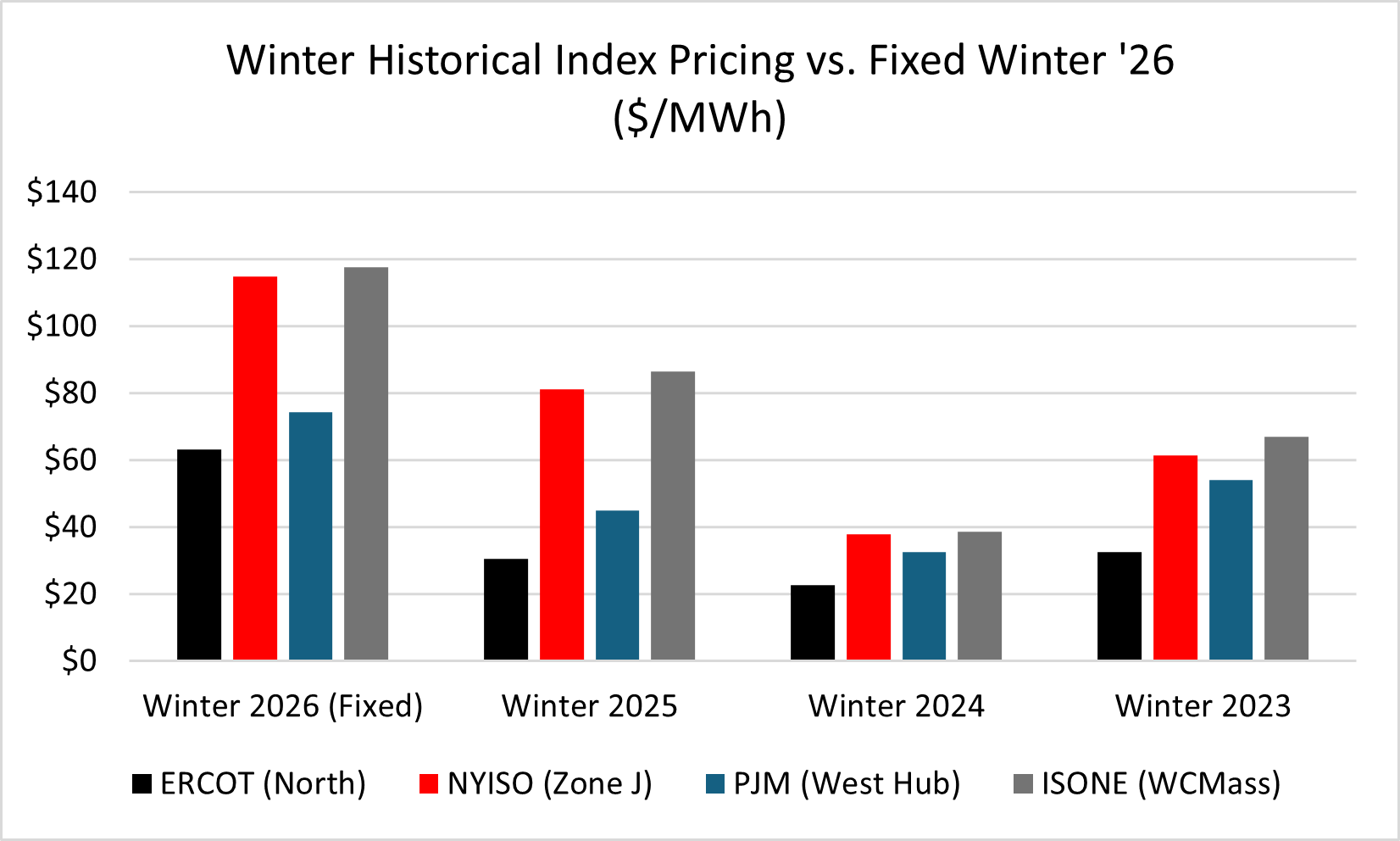

Summer 2025 real-time pricing for NYISO increased 56% vs. summer 2024, PJM Western Hub increased 35%, ISO-NE increased 27%, and ERCOT increased 16%. These increases across the board have contributed to increased fixed prices for summer 2026 where premiums versus the settled summer index prices range from 25% (NYISO) to 173% (ERCOT). These premiums point to volatile historical index pricing as well as demand growth in these particular ISO’s.

Summer NYMEX natural gas settlements averaged a 39% premium vs. summer 2024, a primary driver for power prices. As a result of elevated natural gas prices along with increased demand, there was an unexpected resurgence in coal generation. For instance, in ERCOT summer 2025 coal generation increased 2.6% year-over-year, whereas in previous years coal generation had been on a consistent decline. The same can be said for PJM where coal generation increased 17% year-over-year, yet had decreased 21% summer 2024 vs. summer 2023.

Summer 2025 was relatively mild with 3% less cooling degree days on a population weighted basis versus summer 2024.

Winter 2026

Winter 2026 is shaping up to be expensive even though forecasts are favorable for a mild season and natural gas inventories are plentiful. NYMEX natural gas winter futures have rallied over the last month, adding about 15% of premium in tandem with spot natural gas’ rally.

October shaped up to be mild with very little heating demand. On a population weighted basis October saw 18% less heating demand days versus the historical norm. November has been mild too with 9% less heating demand two weeks into the month vs. the norm. December through February shows near to above normal temperatures for the vast majority of the country, while the Northwest and Midwest may see some below average temperatures.

Natural gas inventories are about full heading into winter, standing 4.5% above the 5-yr average for this time of year. November marks the official beginning of the natural gas inventory withdraw season. With a considerably mild October and a mild start to November injections to the natural gas inventory have continued with week ending November 7 having an implied flow of +45 Bcf and the possibility of a net injection for the second week in November.

Natural gas production remains near record levels. According to the EIA, 2025 is expected to close out averaging 107.7 Bcf/d in production, compared to 103.2 Bcf/d average for 2024.

All of the above points to an abundant natural gas supply where high supply should be keeping prices in check. This is clearly not the case. The biggest driver in this equation, tightening the supply balance is the massive increase in LNG exports. Current US production, around 108.6 Bcf/d is far exceeding winter 2024 around 105.3 Bcf/d. Comparatively, over the past year LNG feedgas has grown from 14.9 Bcf/d to approximately 18.2 Bcf/d, a 3.3 Bcf/day increase year-over-year. Feedgas is expected to reach 19 Bcf/d by year end, completely erasing the gains made by elevated production. We expect to see LNG feedgas volumes increase as we head into winter. 11/13/25 Golden Pass LNG terminal was granted approval for fuel gas introduction, which is receiving about .0085 Bcf/d, expected to increase to 2.4 Bcf/d at at full capacity in 2027.

In addition to more liquefaction capacity coming online, there will be seasonal increases in LNG exports. US LNG facilities, mostly concentrated in the sweltering Gulf Coast are design to operate at 104° F. At 104° F liquefaction is achieved at approximately 300kWh per ton of LNG. At 50° F liquefaction occurs with about 225kWh per ton, at 14° the same liquefaction is realized with about 180kWh per ton.

We expect to see LNG feedgas break all production records. We believe this aspect of the global natural gas market is the primary driver tightening supply and adding further premium to future contracts.