Infinity Insights - Volume 14, Issue 7

MONTHLY UPDATE - AUGUST 2024 EDITION

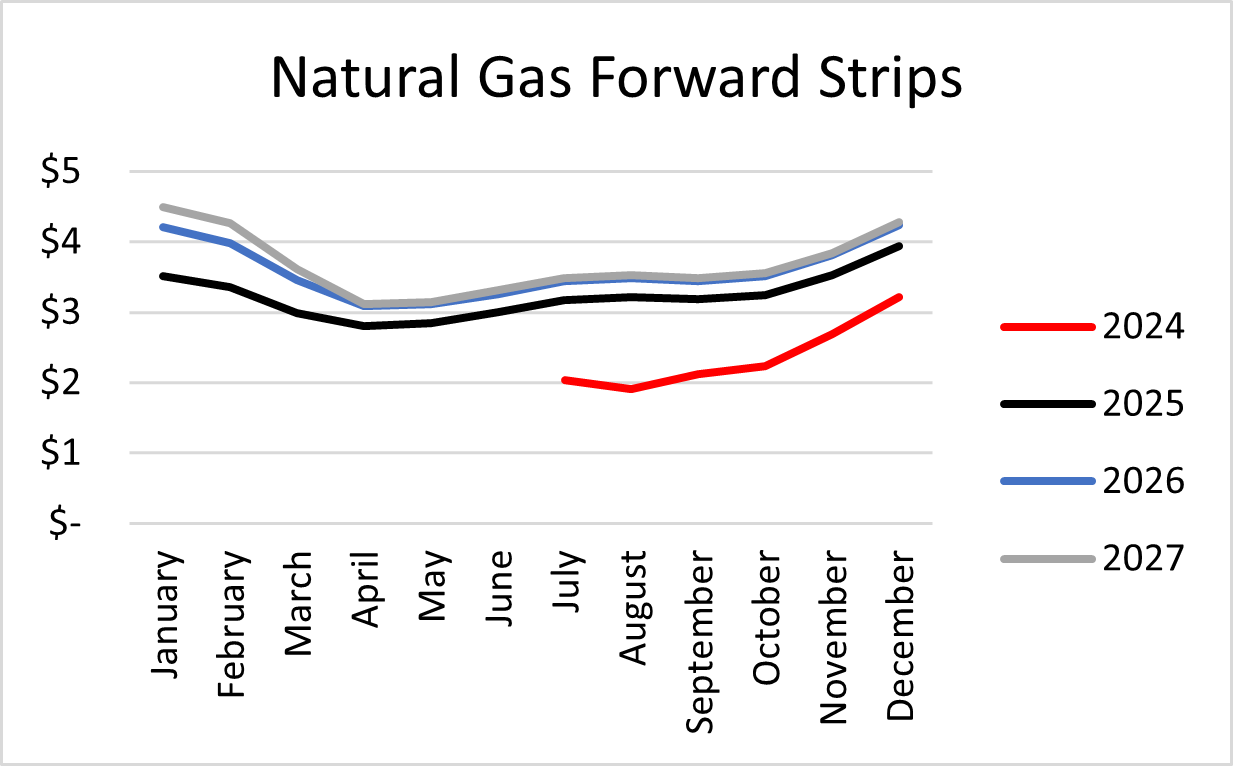

NATURAL GAS

NYMEX Natural Gas has settled down to the $2.10 range with the most recent EIA Weekly Natural Gas Storage Report showing a net injection of 22 Bcf week over week, greater than consensus estimate at 13 Bcf.

Spot month natural gas has support at $2.00 with resistance at $2.50.

Calendar year 2024 finds support at $1.91 with resistance at $3.25. Calendar year 2025 has support at $2.81 with resistance at $3.94, a decrease versus prior month.

Production is strong at 102 Bcf/day on average for July, putting downward pressure on spot pricing. US LNG exports were reduced with Freeport LNG throttling production starting July 7 in anticipation of Hurricane Beryl. Freeport LNG is now back to full capacity.

WEATHER

Year to date, on a US population weighted basis, we have experienced 21% more cooling degree days than the historic norm. Mainly due to the hotter than normal temperatures, the US has generated 5% more electricity 1st half of ’24 vs. 1st half of ’23.

NOAA short-term (6-14 day) and long-term (3 month) forecasts show hotter than normal temperatures for the majority of the continental US.

Atlantic Activity

There is currently one disturbance in the Atlantic. The system is expected to develop into a disturbance later this week with a forecasted trajectory towards Puerto Rico. We are still very early in the system’s development and the trajectory is expected to change as is approaches the British Virgin Islands in the northeastern Caribbean.

Ocean heat content in the main development region remains hot, with current heat content at the level usually observed in the seasonal peak in October. The region’s upward trend has slowed slightly with a solid Saharan Air Layer, 2 tropical storms and 1 major hurricanes stirring up the region. Heat content is close to what was observed late-July 2023. Drought does not appear to be an issue at this time with decent precipitation forecasted.

MARKET NEWS

2024/2025 PJM Capacity Auction Results

PJM recently finalized their 2024/2025 capacity auction. PJM operates in DE, Il, IN, KY, MD, MI, NJ, NC, OH, PA, TN, VA, WV and DC – the largest regional transmission organization (RTO) in the US. PJM is a capacity market, meaning the RTO goes to market with their forecasted generation needs and generators provide commitments to provide certain amounts of generated power in the future at an auctioned price. The RTO then selects the most cost effective and reliable generators and secures contracts for the deliveries, ensuring there is enough capacity to meet future demand.

The most recent auction for 2024/2025 deliveries came in significantly softer than the prior 2024/2025 auction. The clearing price went from $34.13/MW-day to $28.92/MW-day, a 15% decrease. The decrease in clearing price is mainly attributed to a shift in the generation mix. As expected, committed coal resources were the loss leader with a decrease of 2,050 MW followed by hydro at a decrease of 361 MW and then wind at a decrease of 212 MW. The biggest increase came from solar at an increase of 1,301 MW.

Comparatively, Tuesday, July 30th PJM completed its Base Residual Auction for 2025/2026. Clearing price for this auction was $269.92/MW-day, a shocking 800% increase vs. 2024/2025 deliveries. PJM’s CEO Manu Asthana said “the market is sending a price signal that should incent investment in resources”. This is one of the benefits of a capacity market. Generators have a strong sense of future needs and prices and can adjust their generating commitments accordingly. With the latest 2025/2026 results generators are incentivized to make more capacity available. This will increase available capacity and put downward pressure on pricing. The next auction, 3rd Incremental Auction, for the 2025/2026 capacity is scheduled for February 2025 where we expect pricing to fall closer in line to the 2024/2025 results. The 3rd Incremental Auction results, which are expected to be much lower than the $269 cleared July 30th, would then be blended with the $269 rate for a much more palatable rate below the $50/MW range.

Click here to read PJM’s release on the 2024/2025 base residual auction results.

Hurricane Beryl Aftermath – CenterPoint Energy

CenterPoint Energy is being heavily scrutinized because of the utility’s poor performance and lack of preparedness handling Hurricane Beryl. Click here for a special report we released on Hurricane Beryl.

Monday, July 29th Jason Wells, CEO and COO of CenterPoint Energy testified before the Texas Senate Select Committee on Hurricane and Tropical Storm Preparedness, Recovery, and Electricity. Houston Senator Paul Bettencourt didn’t mince words when addressing Jason Wells, asking “what would you say to the average person that you should resign?” Wells responded saying “If I resign today, we lose momentum on the things that are going to have the best possible impact for the Greater Houston region.”

Wells was asked specifically about CenterPoint Energy’s inability to restore its outage tracker prior to Hurricane Beryl, CenterPoint Energy’s delays in a 5-year vegetation management (tree trimming) program, and the usefulness of $800 million worth of mobile generators that have gone unused.

State Senator Bettencourt shared his intention to propose a bill to clawback ratepayer funds used to purchase the unused mobile generators. Governor Greg Abbott has demanded CenterPoint Energy must “articulate to me exactly what they’re going to do to meet my demands by July 31st” or he would encourage the PUC to reject CenterPoint Energy’s request to recover funds utilized to restore electric services lost because Hurricane Beryl. CenterPoint Energy claims they have incurred more than $1.6B in restoration costs between the May derecho windstorm and Hurricane Beryl. During the special committee hearing Houston Mayor John Whitmire stated “I’m upset. I don’t have any more patience. No more excuses. CenterPoint makes a great return, and they’re just going to have to spend it on preparation, operations, and recovery”.

A leadership shakeup is already underway at CenterPoint Energy with the sudden departure of Lyanne Wilson who served as Senior Vice President of Electric Business.

It will be interesting to see how far this investigation goes, how CenterPoint Energy leadership changes and who will be held accountable as light is shed on CenterPoint Energy’s failures in dealing with the region’s most recent natural disaster.

GEOPOLITICS

Venezuela

Venezuelan incumbent president, Nicolas Maduro is claiming victory in the country’s latest presidential election. Maria Corina Machado, Maduro’s opposition leadership is claiming victory as well. Opposition claims 73% of voting results were in favor of Edmundo Gonzalez, Maduro’s opposition. International observers point out a multitude of irregularities in the election results and a severe lack of transparency. Protestors have taken to the street and Maduro has deployed national armed forces to suppress the protests. The protests and conflict have resulted in at least 11 deaths and over 700 people being detained.

Maduro has served as Venezuela’s president since 2013. He was proceeded by Hugo Chavez who was elected president in 1998. During Chavez’s reign industries were nationalized and has remained this way since. Venezuela’s economy has faltered under socialist rule and suffers from high inflation, unemployment and migration from Venezuela. According to the EIA, globally, Venezuela has the largest proven crude oil reserves and 9th greatest proven natural gas reserves. Yet Venezuela ranks 21st and 36th in oil and natural gas production respectively.

We hope to see democracy prevail and a return to capitalism which would surely benefit the general population of this mineral rich nation.

Europe

The European Central Bank (ECB) cut interest rates in June to 3.75%. Rates were held in July. The latest data shows inflation ticked up to 2.6% in July from 2.5% in June. Inflation in Europe peaked in October 2022 at 10.6%. The ECB has done an effective job managing inflation by increasing interest rates. ECB was a leader amongst central banks in cutting interest rates after inflation appeared to be waning. The latest data complicates future rate management as economies try to navigate and achieve a soft landing, balancing inflation and interest rates.

Global natural gas prices ($/MMBtu):

Henry Hub (USA): $2.05

NBP (UK): $9.6

TTF (Dutch) $10.24

JKM (Japan/Korea) $12.32